Santander Prospera

A maior operação de microcrédito do Brasil apresentada em evento da ONU, em NY

Introdução

O Santander Prospera é o programa de microcrédito produtivo orientado do Santander, a maior operação privada do tipo no Brasil. Ele leva crédito a microempreendedores que estão fora do sistema bancário tradicional: donas de pequenos comércios, vendedores ambulantes, trabalhadores informais de periferias e cidades de pequeno e médio porte.

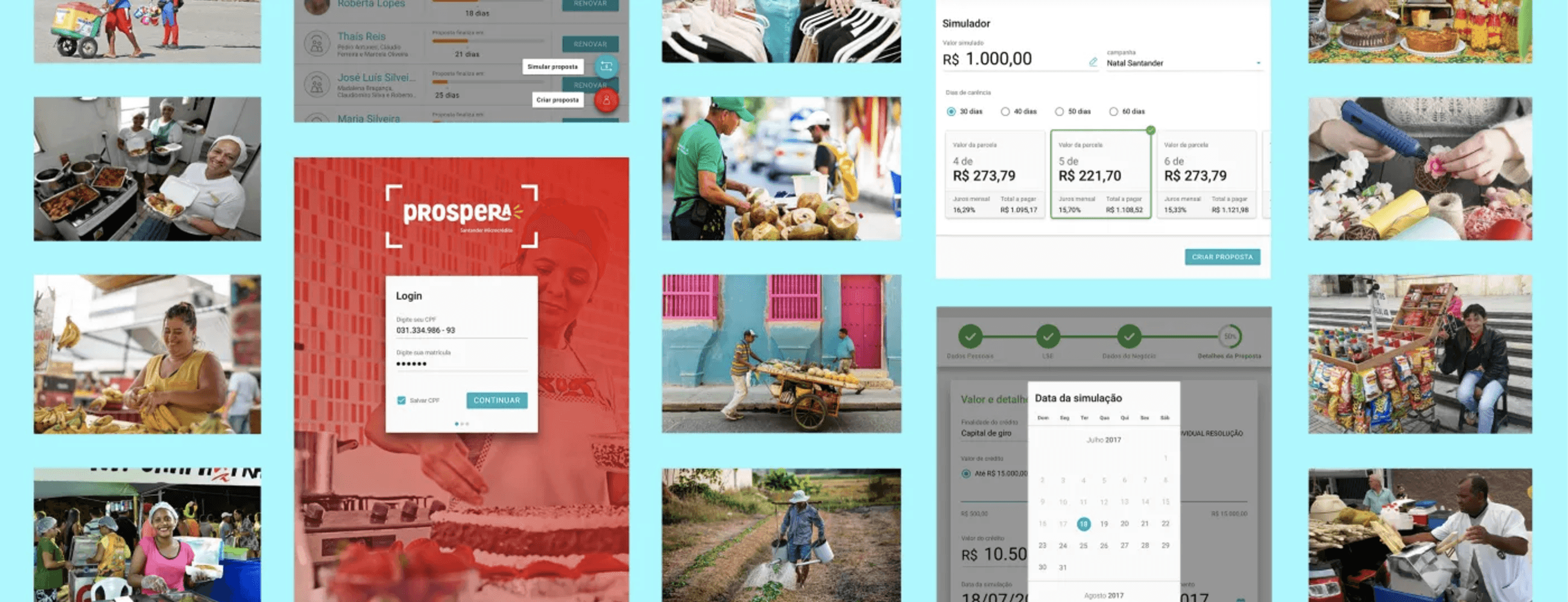

O coração da operação são os Agentes de Crédito (ACs), profissionais que percorrem as comunidades visitando clientes, avaliando negócios e construindo relações de confiança. Mas, enquanto o relacionamento era de alta qualidade, a operação por trás dele era analógica: formulários em papel, retrabalho, sistemas legados desconectados e um ciclo de 5 a 15 dias entre a visita ao cliente e a resposta do banco.

Este case conta como, atuando como UX / UI Designer, ajudei a transformar essa operação em uma jornada 100% digital — um projeto que o Santander já havia tentado resolver antes, sem sucesso, e que desta vez foi entregue, escalado e reconhecido internacionalmente.

O desafio

O desafio tinha três camadas

A camada operacional. O processo de concessão de crédito dependia de papel do início ao fim. O Agente de Crédito visitava o cliente, preenchia formulários à mão, voltava à agência e transcrevia tudo manualmente para os sistemas do banco. Cada transcrição era uma oportunidade de erro, cada erro gerava retrabalho, e o cliente, que muitas vezes precisava do dinheiro para repor estoque na mesma semana esperava até 15 dias por uma resposta.

A camada histórica. Este não era um problema novo para o Santander. O banco já havia tentado digitalizar a operação em iniciativas anteriores, com outros parceiros, sem conseguir chegar a uma solução que funcionasse na realidade do campo. Havia ceticismo interno e uma pergunta implícita pairando sobre o projeto: por que desta vez seria diferente?

A camada humana. Qualquer solução precisaria ser adotada por centenas de Agentes de Crédito espalhados pelo Brasil, com diferentes níveis de familiaridade digital, trabalhando em contextos onde conectividade, tempo e atenção são recursos escassos. Uma ferramenta tecnicamente perfeita, mas que não respeitasse o jeito de trabalhar do AC, seria apenas mais uma tentativa fracassada na lista.

O sucesso, portanto, não era "lançar um app". Era provar que era possível digitalizar a maior operação de microcrédito do país sem quebrar o que a fazia funcionar: a relação entre agente e empreendedor.

Meu papel

Atuei como UX / UI Designer do projeto, com responsabilidade de ponta a ponta sobre a experiência — da pesquisa em campo à entrega das telas para desenvolvimento.

Comecei pelo campo, não pela tela. Fiz imersão nas agências de Paraisópolis, acompanhando o dia a dia dos Agentes de Crédito em visitas reais, e conduzi entrevistas com ACs de seis estados do Brasil. Essa pesquisa revelou um insight decisivo: apesar das diferenças regionais, os problemas eram os mesmos em todo o país, o que significava que uma única solução bem desenhada poderia escalar nacionalmente.

Traduzi a pesquisa em direção. Mapeei as jornadas As-Is e To-Be, desenhei a arquitetura da solução e construí wireframes e designs de alta fidelidade que cobriam todo o fluxo: criação de propostas, captura digital de documentos, simulação de crédito, grupos solidários e educação financeira integrada à jornada.

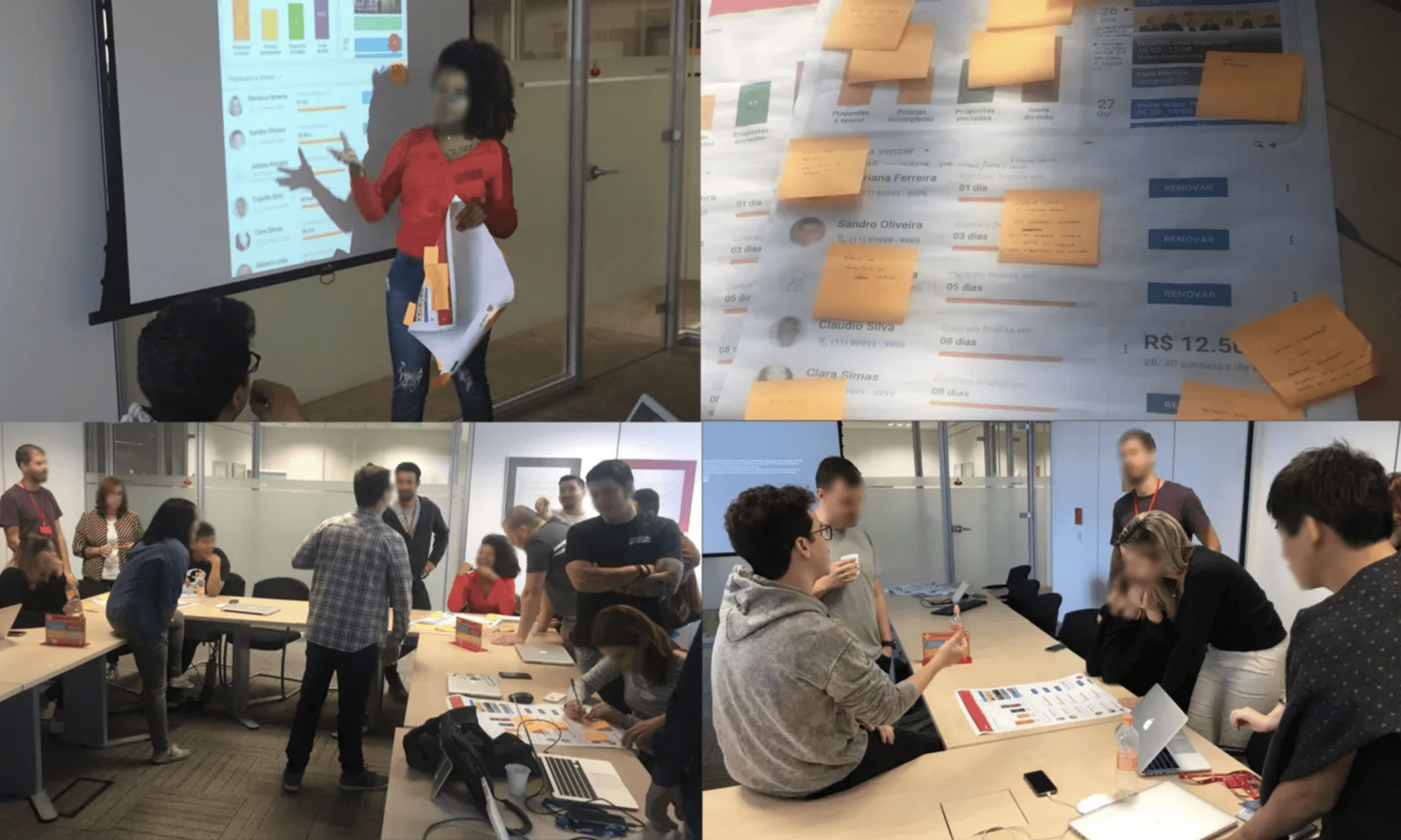

Envolvi os designers do próprio banco. Em vez de trabalhar como um parceiro externo isolado, modelo que já havia falhado antes, fiz questão de trazer os designers internos do Santander para dentro do processo. Facilitei sessões de design critique e workshops de cocriação com eles e com os stakeholders de negócio, risco e tecnologia. Isso garantiu duas coisas: decisões de design mais fortes, validadas por quem conhecia o banco por dentro, e um time interno capaz de sustentar e evoluir o produto depois da entrega.

Trabalhei com velocidade deliberada. Sabendo do histórico de tentativas anteriores, estruturei o trabalho para gerar valor visível rápido: ciclos curtos de pesquisa → definição → desenho → validação com ACs reais. Em poucos meses, saímos do diagnóstico para um produto em desenvolvimento, resolvendo um problema que se arrastava havia anos no banco.

Aprendizados

1. Projetos que já falharam antes exigem mais escuta, não mais pressa. A tentação em um projeto com histórico de fracassos é correr para mostrar resultado. O que destravou o Prospera foi o oposto: entender por que as tentativas anteriores não funcionaram. Elas haviam sido desenhadas para o banco, não para o Agente de Crédito. Quando o campo virou o ponto de partida, a solução encontrou tração.

2. Cocriação não é cerimônia — é estratégia de adoção. Envolver os designers e stakeholders do Santander no processo não foi um gesto de cortesia. Cada workshop transformava potenciais críticos em coautores da solução. Quando o produto chegou ao comitê, ele já tinha defensores dentro do banco.

3. Velocidade vem de decidir cedo o que importa. Trabalhamos rápido não por cortar etapas, mas por priorizar com clareza: digitalizar primeiro o fluxo de proposta (a maior dor), e tratar o resto como evolução. Escopo enxuto e bem fundamentado vale mais que escopo completo e teórico.

4. Em contextos de inclusão financeira, confiança é o requisito número um. Cada decisão de interface: validação em tempo real, status visível da proposta, transparência sobre juros e parcelas, etc… existia para proteger a confiança entre agente, cliente e banco. UX, aqui, não era estética: era a infraestrutura da relação.

Resultados

O reconhecimento veio na mesma proporção do impacto: em setembro de 2018, o Santander foi convidado a apresentar o case do Prospera em evento da ONU, em Nova York, como referência mundial de impacto social e econômico por meio do microcrédito. No ano seguinte, a operação levou o banco ao top 10 do ranking Change the World, da revista Fortune — o primeiro banco brasileiro a figurar nas primeiras posições da lista.

Um projeto que o banco já havia tentado outras vezes virou, em poucos meses de trabalho centrado nas pessoas certas, um case global.

Explore o case completo

No case completo, mostro os bastidores da transformação: as descobertas da imersão em Paraisópolis e das entrevistas com Agentes de Crédito pelo Brasil, as jornadas As-Is e To-Be, as decisões de design por trás de cada fluxo — da proposta 100% digital aos grupos solidários — e como a cocriação com os designers do banco destravou um projeto que já havia falhado outras vezes. Explore o processo completo que levou a maior operação de microcrédito do Brasil a ser apresentada em evento da ONU.

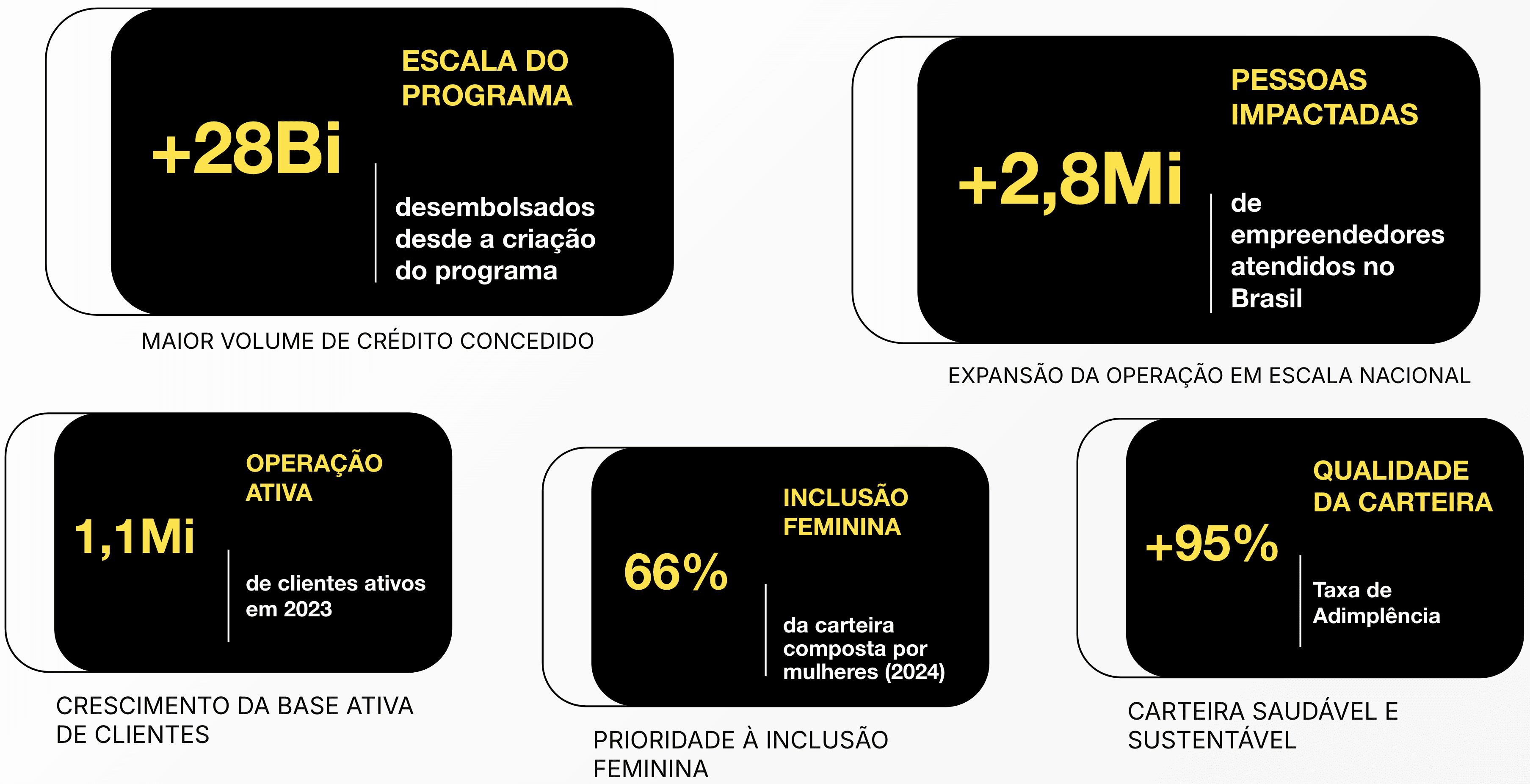

+ R$ 28 Bi

desembolsados desde a criação do programa

+2,8 Mi

de empreendedores atendidos no Brasil

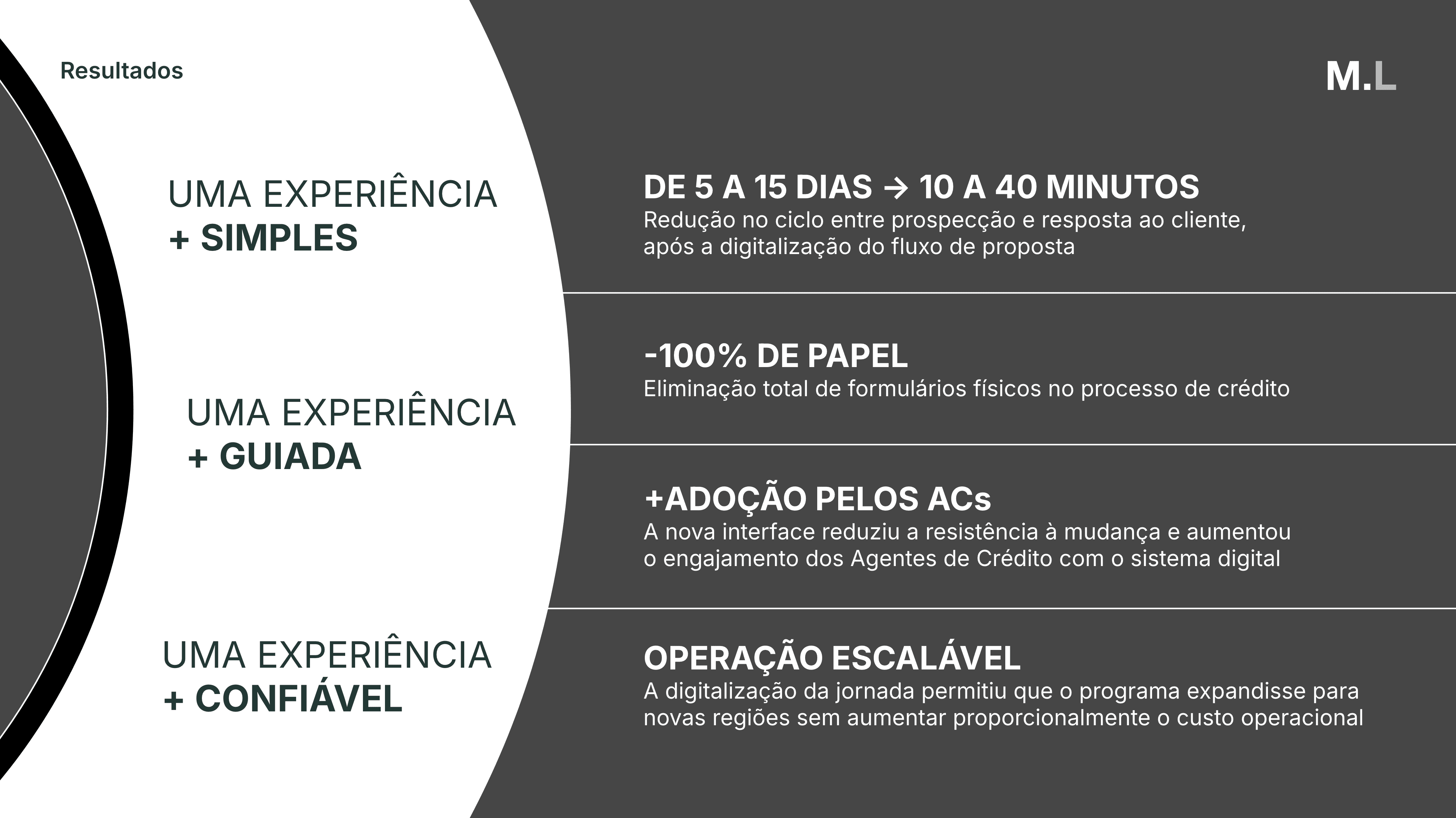

De 15 dias para 10 min

no tempo de criação ou renovação de proposta de crédito